This is the third installment in a series of five posts based on data from the 2016 LSSSE survey administration and the 2016 Annual Report. The LSSSE 2016 Annual Report highlights inequities in scholarship policies and the associated consequences for student loan debt.

Equity is often assumed to be the same as equality, but they are different. Equity accounts for differences in ways that equality does not. In fact, the insensitivity of equality-based frameworks can exacerbate inequity through a dichotomous compounding of privilege and disadvantage. Merit scholarship programs provide a classic example of this phenomenon. Merit scholarships tend to be awarded through equality frameworks, in which similar criteria are applied to all applicants. These criteria most often revolve around standardized test scores and other factors that track closely to non-merit indicators, such as socioeconomic status. In the end, wealth and privilege become proxies for merit, a conflation that results in financial windfalls and further advantages for applicants least in need of such assistance.

We used parental education as a proxy for a respondent’s socioeconomic background in order to compare debt and scholarship trends. Framing socioeconomic background based on parental education is common in the research literature and is rooted in the fact that children of college-educated parents are more likely than other children to come from relatively affluent backgrounds. We classified our respondents into three parental education groupings:

FG-HS: “first-generation” respondents for whom neither parent has more than a high school diploma

FG-SC: “first-generation” respondents for whom at least one parent has some college experience, but no bachelor’s degree

N-FG: “non-first-generation” respondents for whom at least one parent has a bachelor’s degree or higher

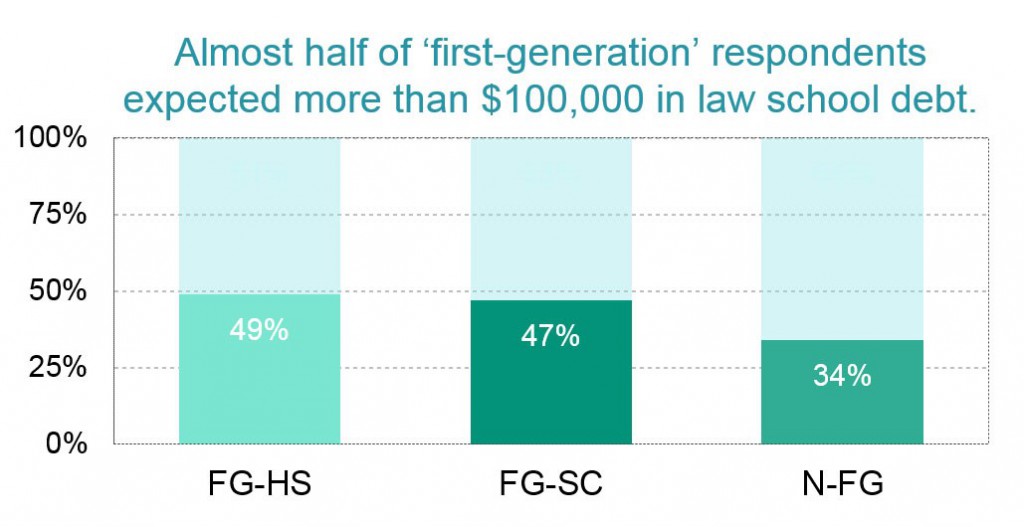

The debt burden is highest among respondents for whom neither parent has more than a high school diploma. Almost half of these “first-generation” respondents (FG-HS) expected to owe more than $100,000, compared to 34% to non-first-generation (N-FG) respondents.

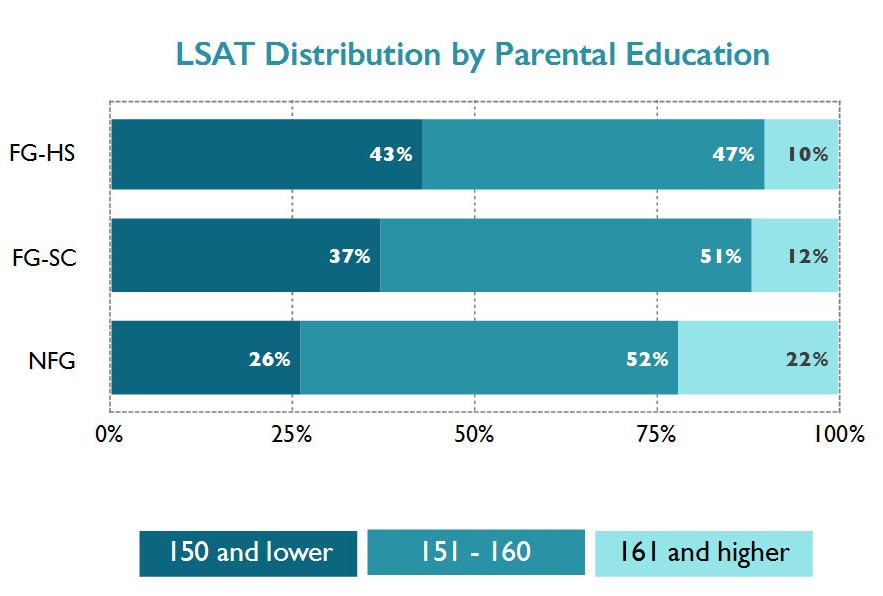

In our sample, N-FG respondents – presumably the most privileged group – were most likely to have received a merit scholarship; FG-HS respondents – the least privileged – were least likely. Like the disparities in scholarship awards among participants with different racial and ethnic backgrounds (see previous post), the disparities among students with differing parental education levels align with LSAT score trends. Forty-three percent of FG-HS respondents had LSAT scores below 151, compared to about a quarter of N-FG respondents. At the other end, 22% of N-FG respondents scored at 160 or higher, compared to just 10% of FG-HS respondents

The question is often posed: Why shouldn’t the LSAT be a primary criterion for determining who gains admission to law school and who receives scholarships? The most basic answer to this question is that the LSAT is designed to be a predictor of first-year law school performance and, in fact, explains roughly 38% of the variance in first-year law school grades. But the LSAT is even less reliable in predicting longer-term outcomes, such as bar exam performance and career success. Despite these limitations, the LSAT remains a central factor in most admissions and scholarship awarding decisions. It is an unfortunate and uncomfortable truth that a large number of admissions and merit scholarship decisions are rooted in a fundamental misuse of the LSAT. The heavy reliance on LSAT scores to award scholarship money exacerbates disadvantages based on privilege by distributing resources inequitably. Equity requires that we encourage the success of all our students by appreciating their differences and meeting their needs to the extent possible.

In our next post in this series, we will show some interesting associations between the type of scholarship students receive and their expected student loan debt levels.